ATTENTION: The Property Dream Is Quietly Turning Regular People Into Prisoners…

“New Book Reveals How To Build Generational Wealth Without Buying Property or Using Debt."

Written by Entrepreneur & Bestselling Author Lloyd J. Ross

Frances Perez says:

"Value value value. I personally would recommend this book to people on all budgets and incomes. Thank you Lloyd J. Ross for saving me 20 years!"

Steve Long says:

“I am courage people to get this book the YOUNG PEOPLE!!!!!! And read this and follow this plan you WILL LOVE IT”

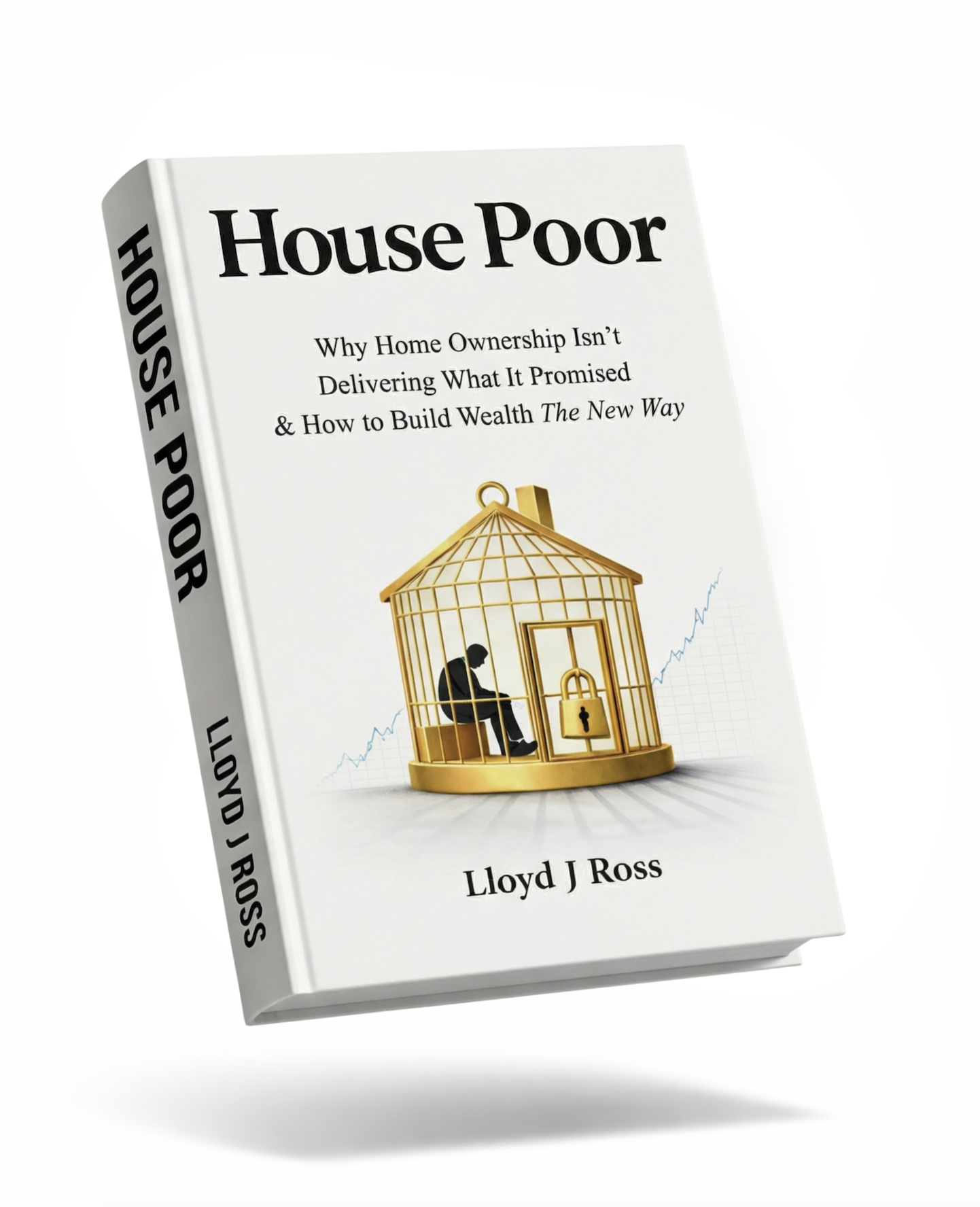

HOUSE POOR

'Why Home Ownership Isn't Delivering What It Promised and How to Build Wealth The New Way'

Lloyd J Ross leads a new approach to building wealth that flips the script on everything you’ve been told about property as the “safe” path — revealing how equity can create the illusion of wealth while quietly reducing freedom.

For decades, buying a home was sold as the safest path to wealth.

Work hard.

Buy property.

Watch it double.

Retire secure.

It worked.

Until it didn’t.

And almost nobody has adjusted their thinking.

Right now, thousands of people with good incomes, respectable careers, and “successful” lives are quietly feeling something they can’t say out loud.

Their mortgage isn’t building freedom.

It’s compressing their life.

They don’t feel rich.

They feel tight.

They feel stretched.

They feel one rate rise, one job shock, one major repair away from panic.

And the worst part?

On paper, they look wealthy.

The Illusion Nobody Talks About

There’s a strange modern condition spreading through the world.

High income.

Nice suburb.

Big loan.

Minimal breathing room.

You’ll hear it phrased like this:

“It’s tight but doable.”

Or:

“We’ve got plenty of equity… it’s just all tied up.”

Or quietly, late at night:

“Did we overpay?”

“Should we have waited?”

“WTF have I done?”

The problem isn’t that people are lazy.

Or irresponsible.

The problem is they’re making 30-year financial decisions based on a 50-year boom that cannot repeat.

Interest rates fell for decades.

Credit expanded.

Population grew.

Asset prices rose in a tailwind environment.

That environment is gone.

But the belief system remains

House Poor

Why Home Ownership Isn’t Delivering What It Promised And How To Build Wealth The New Way

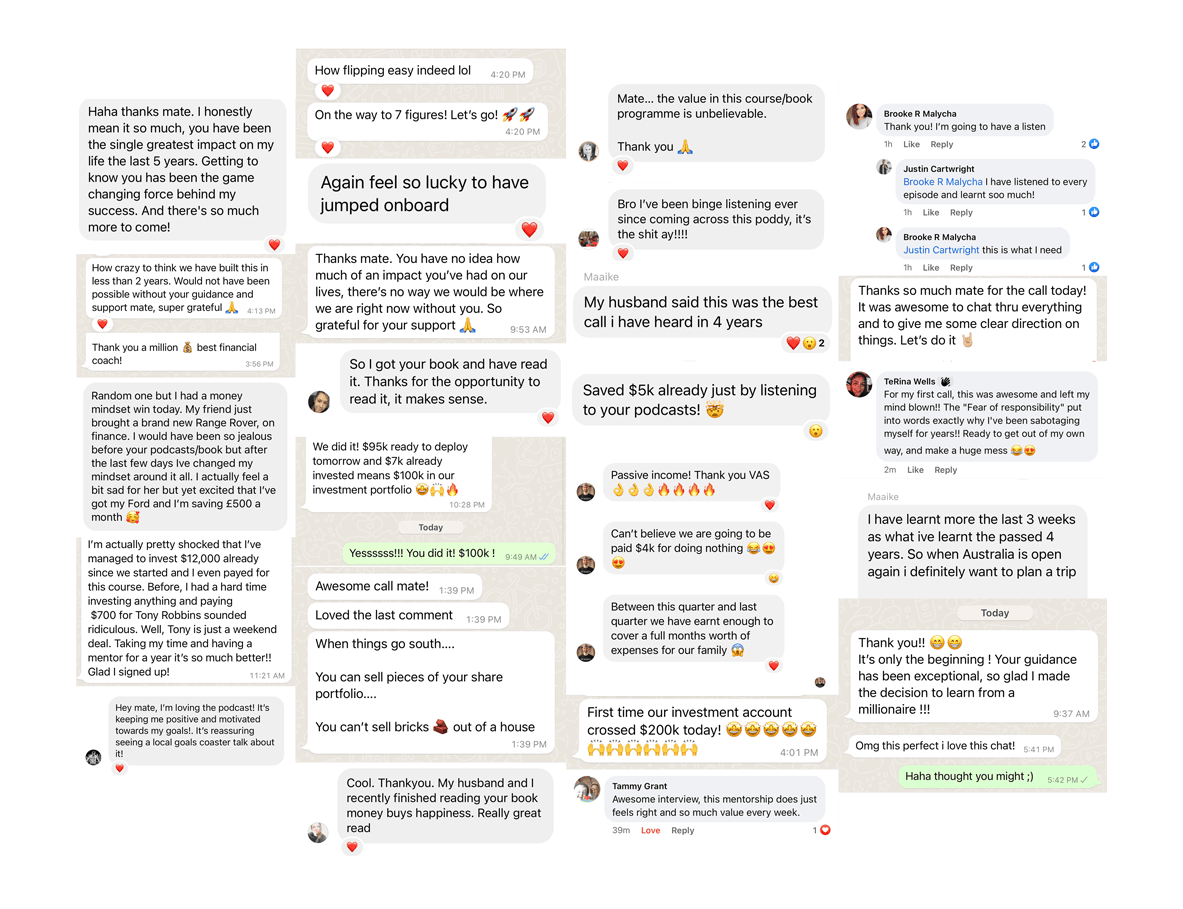

“Read your book on the plane. The simplest and best analogies I have ever seen to do with creating wealth. You are definitely destined for greatness, the level of which is to be determined by you.”

“Just finished your book 🔥🔥🔥🔥🔥🔥

I want to get to $200k ASAP now 😂 it seems so doable.”

“Seriously phenomenal book. I’m going to read it again while implementing it and going to work towards my first money tree. Thank you Lloyd!!

One of the best books on money that I have ever read.”

“Thanks brother. By the way! I became debt-free and started building my money tree!

Thanks for the book you wrote on this Lloyd!”

“Value value value. I personally would recommend this book to people on all budgets

and incomes. Thank you Lloyd J. Ross for saving me 20 years!”

This book was not written by a renter complaining from the sidelines.

It was written by someone who entered the property system at 20.

Real estate licensed.

Property lawyer by 23.

Worked on major international developments.

Spent years inside the machine.

And then stepped back.

Because when you see how the system works from the inside, something becomes obvious:

You cannot live off equity.

You can only live off cashflow.

Equity feels good.

It looks impressive.

It photographs well.

But it doesn’t buy groceries.

It doesn’t give you optionality.

It doesn’t allow you to leave a job you hate.

Cashflow does.

The Brick Prison

There’s a phrase in the book that hits hard:

The Brick Prison.

It doesn’t look like a prison.

It looks like a dream home.

But slowly, subtly, it reduces your options.

You hesitate before changing careers.

You delay starting a business.

You stay in a role that drains you.

You postpone risk.

You shrink your life to protect the mortgage.

You tell yourself it’s temporary.

You tell yourself it’s building wealth.

But 5 years pass.

Then 10.

And your best energy went to servicing debt.

Not building freedom.

The Hidden Cost Iceberg

The mortgage is only the visible tip.

Below the surface?

Insurance increases.

Maintenance shocks.

Interest-heavy repayments.

Transaction costs.

Upgrades you feel socially pressured to make.

Something is always breaking.

Something is always due.

And the psychological weight compounds.

It’s not dramatic enough to collapse.

It’s just heavy enough to exhaust you.

The Moment It Cracks

For some, it happens when rates rise.

For others, when a job becomes unstable.

For many, it’s that first repayment that is almost entirely interest.

That’s when the question lands:

Is this actually building wealth… or just trapping me in a high-status cage?

That moment is what this book is designed to prevent.

Or help you recover from.

Introducing...

The House Poor vs Freedom Framework™

At the heart of this book is a simple decision lens.

Two paths.

One leads to being 'asset-rich' and cashflow-tight.

The other leads to income-producing assets, optionality & freedom.

House Poor

Break Free From The Modern “House Poor” Trap and Build Real Financial Freedom Through Cashflow-Producing Assets — Without Waiting Until 65.

What You'll

Discover Inside

✅ Why the 50-year property boom was driven by forces that cannot repeat

You’ll uncover how falling interest rates, expanding credit, favourable tax policy, and demographic tailwinds created a once-in-a-generation surge in property values. These structural forces worked in one direction for decades — and mathematically cannot repeat. What most people think was “guaranteed growth” was actually a macroeconomic anomaly.

✅ The psychological trap that keeps smart people over-leveraged

You’ll see how cultural conditioning, status signalling, and fear of missing out quietly push even intelligent earners into overstretching. The house becomes a symbol of success — even if it reduces flexibility and increases stress. The trap isn’t stupidity — it’s social programming.

✅ Why “equity growth” often disguises financial fragility

On paper, rising equity feels like progress. In reality, it can mask thin cashflow, high debt exposure, and zero liquidity. The book explains why being “asset-rich” can still mean living financially fragile — especially when your wealth is locked behind repayments and market cycles.

✅ The math behind cashflow-first wealth building

Instead of hoping capital gains rescue you, you’ll learn why income-producing assets change everything. The book breaks down why dividends, business income, and yield-based assets create stability and optionality — regardless of market direction. Cashflow doesn’t require you to sell your future to fund your present.

✅ How to evaluate whether you’re building security or just servicing debt

You’ll learn how to assess your real financial position beyond net worth theatre. Are your assets producing income — or just requiring repayment? The distinction between “ownership” and “control” becomes clear.

✅ What freedom actually looks like in asset form

Freedom isn’t a postcode or a valuation figure — it’s optionality. The book shows what financially flexible living looks like: low fixed costs, income diversity, and the ability to make life decisions without mortgage pressure. True wealth is the ability to choose.

This Is Not Anti-Home

Owning a home isn’t the problem.

Blind leverage is.

Over-commitment is.

Basing your entire financial future on capital gains is.

There are scenarios where buying makes sense.

There are scenarios where renting and investing makes more sense.

The danger is assuming there is only one socially acceptable path.

A Different Way

At 42, Lloyd owns no home.

Instead, he built a $3M share portfolio.

Built multiple cashflow businesses.

Has no mortgage.

Lives off income.

Not theory.

Not Twitter threads.

Real assets.

Real dividends.

Real optionality.

Freedom isn’t about where you live.

It’s about whether your life decisions are dictated by repayments.

Is This Right For You?

The person about to buy and feeling stretched

The new homeowner with quiet regret

The established owner feeling compressed

The high earner wondering why it still feels tight

It’s not for someone looking for property hype.

It’s for someone willing to question it.

A $12 Insurance Policy Against a Million-Dollar Decision

Buying property is often the biggest financial decision of your life.

Yet most people never deeply examine the underlying assumptions.

For $12, you get:

Clarity.

Perspective.

A framework.

And the confidence to choose consciously.

Not emotionally.

Not socially.

Not fearfully.

Consciously.

Two paths.

House Poor.

Or Free.

You don’t just drift into freedom.

You decide.

Frequently Asked Questions (FAQs)

What if I’m about to buy?

Then this may be the highest-ROI $12 you ever spend.

Before committing to a 30-year obligation, you should understand the structural, psychological, and financial forces at play. This isn’t about fear — it’s about clarity before you sign.

Is this just another “renting is better than buying” argument?

No.

This book isn’t anti-homeownership. It’s anti-blind leverage.

There are situations where buying makes sense. There are situations where renting and investing make more sense. The book gives you the framework to decide consciously — instead of following a cultural script.

Are you saying property won’t go up anymore?

No.

Property may still rise in certain areas and cycles.

The argument is that the 50-year tailwinds that fuelled explosive growth — falling interest rates and expanding credit — cannot repeat in the same way. Betting your entire financial future on capital gains is very different from understanding the macro forces behind them.

I already own a home. Is it too late for me?

If you already own a home, then this book is especially valuable if you already feel stretched. It helps you evaluate your real position — not just your equity — and shows how to rebuild optionality from where you are now.

How quickly can I apply what’s inside?

Immediately.

You’ll be able to evaluate your position, your exposure, and your optionality as soon as you finish reading. The framework is simple — but the clarity it creates can change major decisions fast.

What makes Lloyd qualified to write this?

Lloyd worked inside the property system as a real estate professional and property lawyer, saw how leverage cycles operate, and then chose a different path. He built income-producing assets instead of relying on home equity — and lives the framework he teaches.

This isn’t theory. It’s lived strategy.

About Lloyd J Ross

Lloyd J Ross entered the property world at 20, earned his real estate license, and became a property lawyer by 23. He worked inside major developments and saw firsthand how leverage cycles, credit expansion, and buyer psychology truly operate.

From the inside, property looks very different.

He watched rising values create the illusion of wealth while repayments quietly dictated careers, risk tolerance, and life decisions. That tension led him to ask a harder question: is this building freedom — or just status?

Instead of following the same path, Lloyd chose differently. He built a multi-million-dollar share portfolio, created income-producing businesses, and focused on assets that generate cashflow rather than relying on capital gains.

At 42, he owns no home — by design.

Not because he couldn’t. Because he understands the difference between ownership and freedom.

His work challenges financial conditioning and helps people build wealth structures that create optionality, not obligation. House Poor isn’t an attack on property — it’s a call to think clearly about what wealth actually is.

Because true wealth isn’t a valuation figure. It’s the ability to choose.

© Copyright 2026 House Poor. All rights reserved.